An Introduction to TradingPipeline.jl

2024-12-27

I am unsure about how algorithmic trading systems should be structured, so I have been doing a lot of exploring.

Instead of making a framework, I decided to write small libraries that do specific tasks.

They still needed to be joined together in a cohesive way, and I had no clue how to do that until I saw Lucky.jl.

Although TradingPipeline.jl is quite different from Lucky.jl in many ways, it is nevertheless influenced by how it used Rocket.jl to connect async tasks together.

Before I saw his work, I was stuck on the problem of how to organize this data flow for YEARS.

It was a huge revelation for me, so thank you, Olivier.

Introduction to Strategies

Questions of how to open a position (limit orders vs market orders), where to put and move stop losses, position sizing, etc. will be answered by other parts of the code ...eventually.Goals

Portability between exchanges / Exchange agnostic

Relative ease of implementation

To achieve these two goals, I decided to make strategies only responsible for answering 4 questions,

When should a long position be opened?

When should a long position be closed?

When should a short position be opened?

When should a short position be closed?

Furthermore, if you want to write a long-only strategy, just don't implement the *_short functions, and a catch-all will default them to false.

Interface

import TradingPipeline as TPTP.should_open_long(strategy::AbstractStrategy)TP.should_close_long(strategy::AbstractStrategy)TP.should_open_short(strategy::AbstractStrategy)TP.should_close_short(strategy::AbstractStrategy)TP.load_strategy(strategy::AbstractStrategy; kwargs...)

Example: TradingPipeline.HMAStrategy

import TradingPipeline as TP

using OnlineTechnicalIndicators # HMA

using TechnicalIndicatorCharts # Chart

using ReversedSeries # ReversedFrame, crossed_up, crossed_down

mutable struct HMAStrategy <: TP.AbstractStrategy

# You can put whatever state you want inside your strategies.

# For me, the bare minimum is the chart it's using for data,

# and a reversed view of its DataFrame. If you're in to

# multi-timeframe analysis, feel free to use as many charts

# as you want.

chart::Chart

rf::ReversedFrame

function HMAStrategy(chart)

new(chart, ReversedFrame(chart.df))

end

end

function TP.should_open_long(strategy::HMAStrategy)

# if we're neutral and

crossed_up(strategy.rf.hma330, strategy.rf.hma440)

end

function TP.should_close_long(strategy::HMAStrategy)

# if we're long and

crossed_down(strategy.rf.hma330, strategy.rf.hma440)

end

"""

Initialize a long-only 330/440 HMA cross strategy.

Return a chart_subject and strategy_subject.

"""

function TP.load_strategy(::Type{HMAStrategy}; symbol="BTCUSD", tf=Hour(4))

hma_chart = Chart(

symbol, tf,

indicators = [

HMA{Float64}(;period=330),

HMA{Float64}(;period=440)

],

visuals = [

Dict(

:label_name => "HMA 330",

:line_color => "#26c6da",

:line_width => 2

),

Dict(

:label_name => "HMA 440",

:line_color => "#64b5f6",

:line_width => 3

)

]

)

all_charts = Dict(:trend => hma_chart)

chart_subject = ChartSubject(charts=all_charts)

strategy = HMAStrategy(hma_chart)

strategy_subject = StrategySubject(;strategy)

return (chart_subject, strategy_subject)

endRunning a Simulation

The Setup: Do This Once

# load modules

using CryptoMarketData

using TechnicalIndicatorCharts

using ReversedSeries

import ExchangeOperations as XO

using UnPack

using LightweightCharts

import TradingPipeline as TP

import HierarchicalStateMachines as HSM

using TradingPipeline

using TradingPipeline: simulate, GoldenCrossStrategy, HMAStrategy, df_candles_observable

using TradingPipeline: load_strategy, report

# get data

pancakeswap = PancakeSwap()

btcusd1m = load(pancakeswap, "BTCUSD"; span=Date("2023-07-01"):Date("2024-11-29"))

candle_observable = df_candles_observable(btcusd1m)Actually Running the Simulation

@unpack simulator_session, chart_subject = simulate(candle_observable, HMAStrategy);

rdf = report(simulator_session)You can rerun those last 2 lines as many times as you want. Once all the setup before that is done, you don't have to repeat it. Data loading is usually the slowest part of this process, but you don't have to do it often. Once you have that candle_observable, you can keep reusing it over and over again.

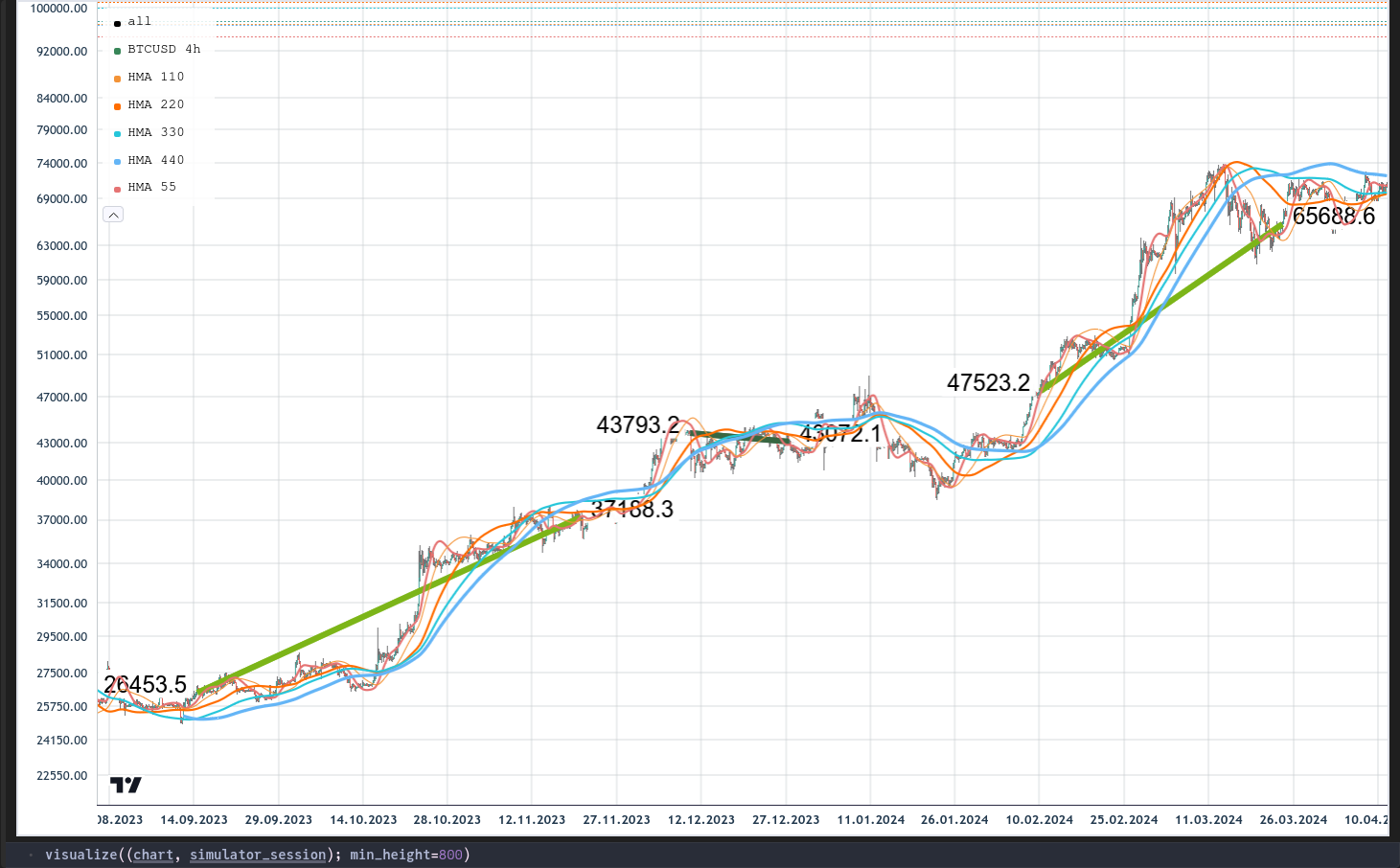

Visualizing Your Trades

The chart_subject can often have multiple charts in it, but in this case we only have one. To visualize it together with the trades that were executed, do this:

chart = chart_subject.charts[:trend]

visualize((chart, simulator_session); min_height=800)

# Multiple dispatch is such a win.

# Respect to whomever came up with this idea in the first place.

It doesn't matter what timeframe the charts are in. Even if the chart you give it doesn't have the exact timestamp the trade entered and exited on, it'll try to get as close as the chart's timeframe allows and draw the lines accordingly.

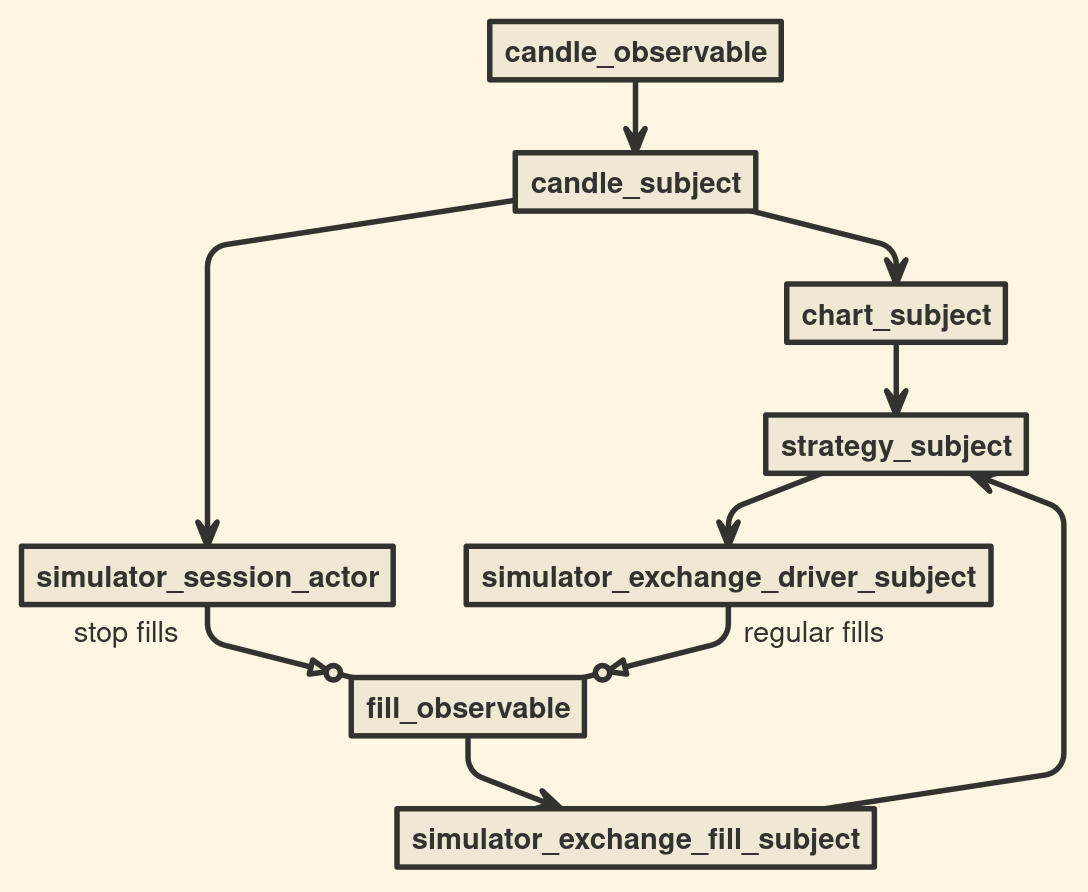

My Simulation Pipeline

This is how data flows while simulate is running.

candle_observableis currently backed by a DataFrame for backtesting.If I wanted to do livetesting, it could be backed by a websocket.

If I wanted to do live trading,

simulator_session_actorgoes away.simulator_exchange_driver_subjectgets swapped out for a real exchange driver.simulator_exchange_fill_subjectalso gets swapped out for an exchange-specific implementation.

ChartSubject

This consumes

Candles and incrementally builds as many charts in as many timeframes as you want.I treat its contents like shared memory, but by gentleman's agreement, only

ChartSubjectis allowed to write to the charts.Everyone else just reads, and so far, it's only the strategy that's looking.

StrategySubjects

This consumes data from two sources.

Tuple{Symbol, Candle}notifications from ChartSubject.ExchangeFillnotifications from an ExchangeFillSubject.

Its job is to manage the lifecycle of a trade using a Strategy.

The state machine you see above is managing the lifecycle of a trade.

This was actually the simplest state machine I could make for this task.

It assumes market orders will open and close positions with complete fills.

Stop orders are also assumed to completely close a position.

More elaborate state machines may be created in the future if people want to do things like:

Take partial profit during the lifetime of a trade

Use limit orders instead of market orders to open and close positions

Reverse a position with a large order that simultaneously closes the current position and opens a new one

Open a position with a stop order

For now, though, let's keep it simple.

ExchangeDriverSubjects

It consumes messages of type

TradeDecision.Tfrom the StrategySubject.The actual API calls to create orders that open or close a position comes from here.

There is currently only one called

SimulatorExchangeDriverSubject.It is really dumb.

It hard codes the position size to 1.

Every supported exchange will have at least one driver.

Some exchanges may have more than one driver.

For example, if you want to use limit orders instead of market orders, that would require a different driver even though you're using the same exchange.

I'm thinking of putting a lot of responsiblities here or in adjacent Rocket subjects that have yet to be written.

Position sizing decisions will probably happen here.

Stop loss management may be adjacent to this.

ExchangeFillSubjects

This consumes exchange-specific fill messages and translates them to more generic fill messages before sending them back to the StrategySubject.

There is currently only one called

SimulatorExchangeFillSubject.Every time you try to open or close a position, you want to make sure you get an acknowledgment from the exchange that it went through before moving on.

That's why the state machine from the StrategySubject makes a distinction between wanting to be long versus actually being long.

Also, stop losses are often hit at unpredictable times, so this will let the StrategySubject know when that happens so that it can change its state appropriately.

I have a lot more work to do.

As I got further down the document, the code I described became less and less mature.

The biggest reason for that is that it's newly explored territory for me.

Until I started using Rocket.jl, I couldn't really explore this area, so I'm just now starting to put serious thought into how this part of the pipeline should work.

If you've made it this far, thanks. It's a lot to read, but I tried to make it as easy to take in as I could.